*Disclosure: I don't hold or plan to trade any of the securities mentioned in this blog within the next 72 hours.

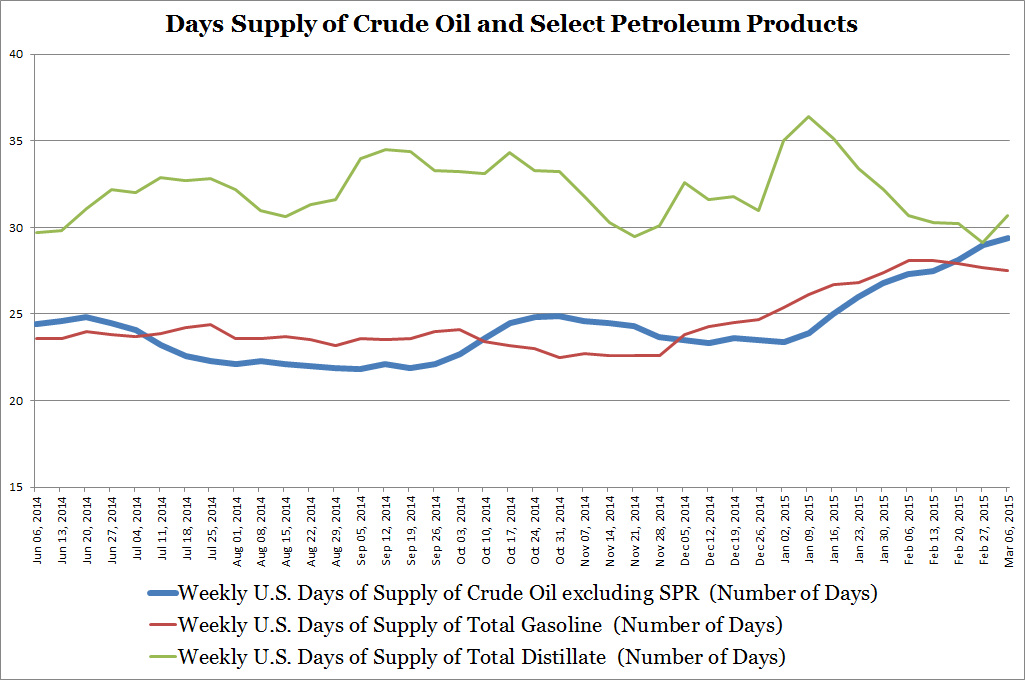

Since June 2014, crude oil prices have fallen from over $100/barrel to around $50/barrel. While the Energy Information Administration (EIA) confirms that U.S. crude oil production continues to rise from 8.4 million barrels/day in June 2014 to 9.3 million barrels/day in March 2015. The chart below illustrates the increasing oversupply of crude oil. Gasoline and distillate supplies which are more centered on refining shows a mixed story. Gasoline supplies seems correlated with crude oil supply while distillate supplies move in the opposite direction.

Source: EIA

In terms of industry employment, the Bureau of Labor Statistics reports oil and gas extraction employment went from an all time high of 201,000 workers in October 2014 to 198,300 in February 2015 while petroleum and coal products employment followed with a drop from 110,700 workers to 106,500 in the same period The energy industry as represented by the Energy Select Sector SPDR ETF (XLE) has fallen around 25% since June 2014.

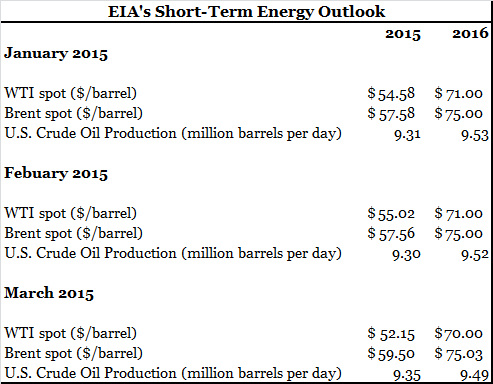

The Energy Information Administration (EIA) released their March Short-Term Energy Outlook this week. I have select data organized below. Current crude oil prices are expected to remain in the $55/barrel range this year before rising in 2016. The only noteworthy estimation change in the last two months is that 2015 U.S. crude oil production is increased 2016 production is cut.

The Energy Information Administration (EIA) released their March Short-Term Energy Outlook this week. I have select data organized below. Current crude oil prices are expected to remain in the $55/barrel range this year before rising in 2016. The only noteworthy estimation change in the last two months is that 2015 U.S. crude oil production is increased 2016 production is cut.

Source: EIA

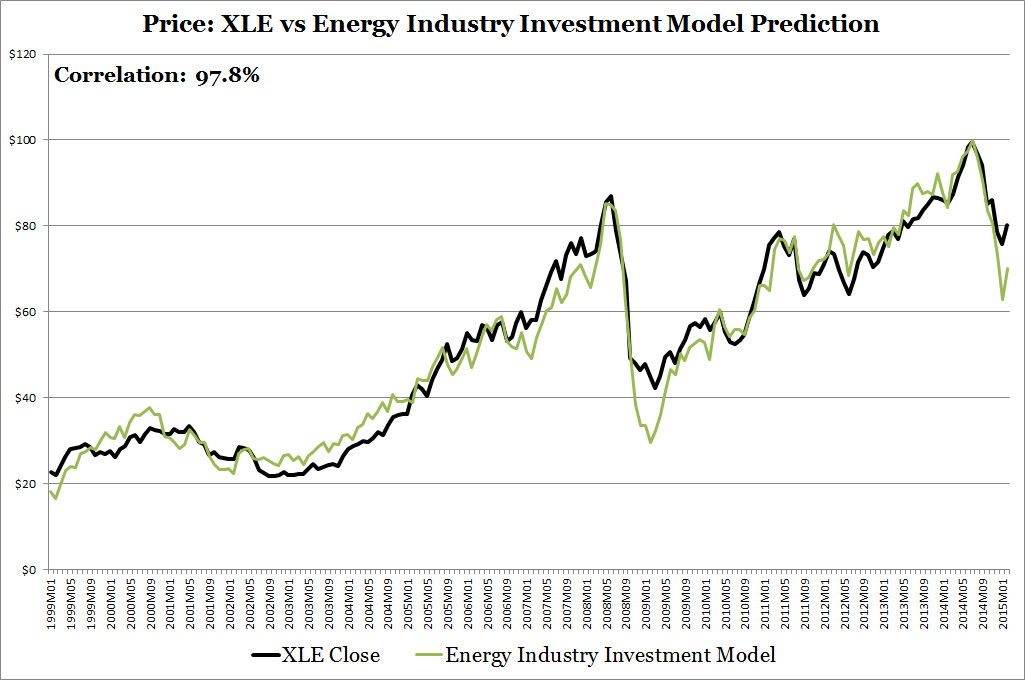

Predicting the performance of the Energy Select Sector SPDR ETF (XLE) is difficult, however, I built the Energy Industry Investment Model to help estimate XLE's price based on historical relationships with crude oil/petroleum products production, crude oil prices, and stock market performance. The model's estimated price has a 97.8% correlation with XLE's price since 1999.

Sources: EIA, World Bank, Yahoo Finance

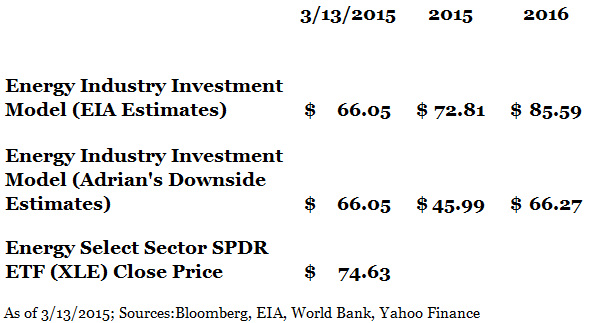

The Energy Industry Investment Model estimates that XLE is currently worth $66.05 while XLE is at $74.63. See below table. EIA's Short-Term Energy Outlook data is integrated into the model for 2015 and 2016 results. Although the EIA tries their best to project the energy industry's future, nobody has a crystal ball. Therefore, I'm also proposing a downside scenario below due to forecast uncertainty.

- Stock Market Performance declines 5% from current levels and stays there for 2015 and 2016 due to fears that Feds will increase interest rates, a sluggish global economy, and a growing U.S. economy.

- Oil Prices move down to $30/barrel in 2015 and rise back to $50/barrel in 2016. This assumes that lower oil price is necessary to reduce crude oil supply and that $50/barrel is here to stay for 2016 as increases in prices will incentivize idled rigs to resume production.

- Crude Oil and Petroleum Product Production return to June 2014 levels in 2015 (a drop of approximately 6%) but bounces back at EIA's 2015 growth rate for 2016 The production drop in 2015 due to oil's price drop(point 2) will allow excess crude oil inventories to be refined.

Should you pull the trigger? Using EIA's estimate in my model says that longer term investors should buy and hold until the energy industry recovers in 2016. My downside scenario, not likely to occur and playing devil's advocate, suggests that the worst isn't over. I'm a relatively cautious investor therefore I'm subjectively assigning a 20% probability that my downside scenario might happen. Using the weighted probability, the estimated price is now $67.44 for 2015 and $81.73 for 2016. I suggest investors buy XLE at or below $67/share and wait for a recovery next year.

RSS Feed

RSS Feed