Source: Yahoo Finance

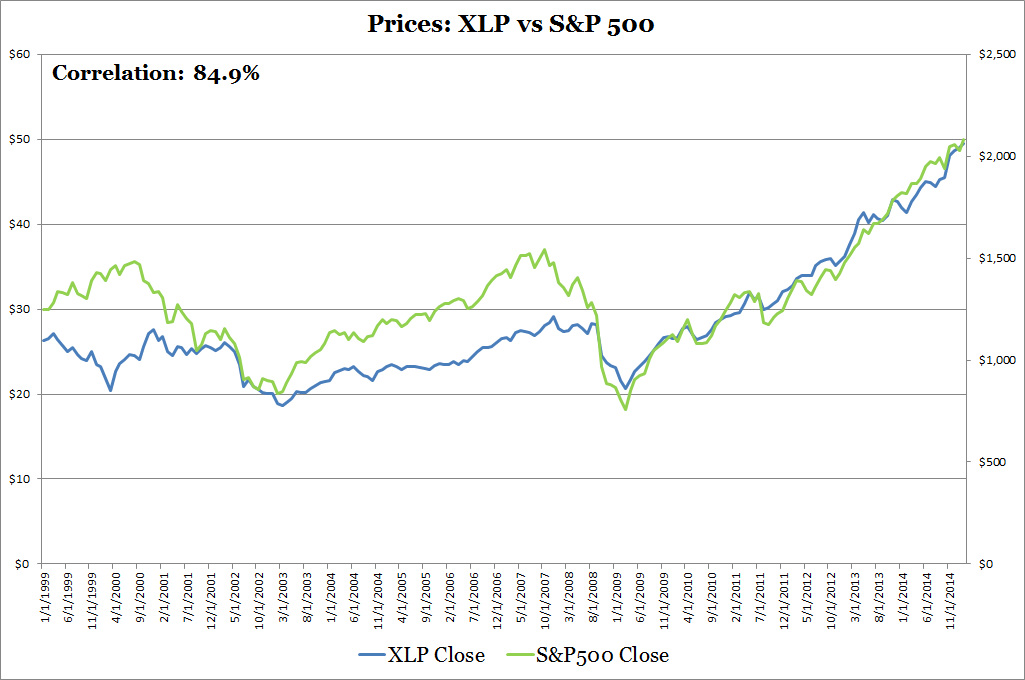

Recently, the U.S. Consumer Staples Industry as represented by the Consumer Staples Select Sector SPDR ETF (XLP) as well as his friend the S&P 500 are struggling for direction. It's important to look at the S&P 500 as stocks are influenced by the overall stock market especially with significant XLP's large cap membership. Historically, the pair have had distance between them. During the Dot Com era they moved oppositely, while during the mid 2000s, XLP lagged the S&P 500 for several years. Since the Great Recession, XLP and the S&P 500 are best friends.

Source: Yahoo Finance

Is The Consumer Staples Industry Just Spinning My Wheels? We'll look at at both industry and macroeconomic level data to find where the industry is heading:

Industry Level Data

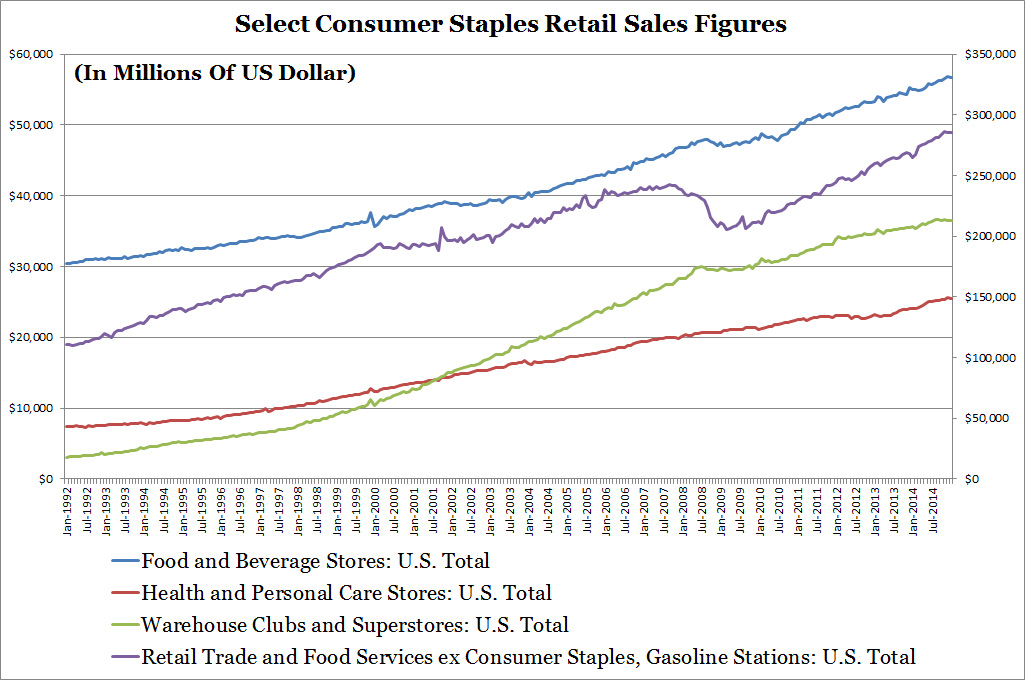

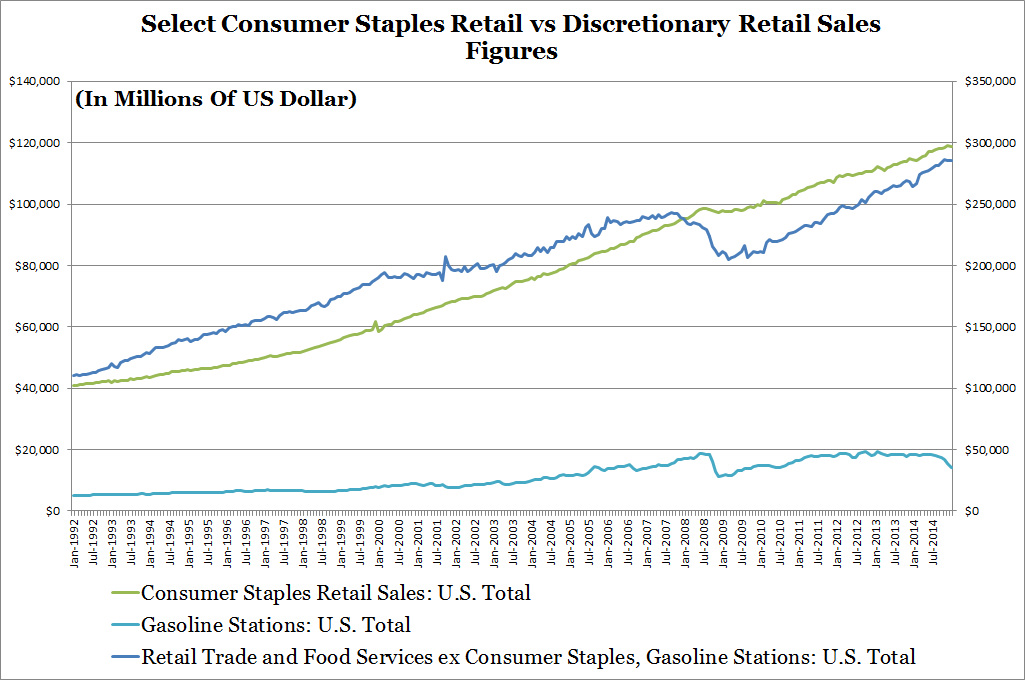

Industry Data is supportive of growth as the National Retail Federation expects retail sales to grow 4.1% in 2015, on top of last year's growth of 3.5% last year. Although my charts below for Retail Trade and Food Services does include automobiles and restaurants, I see automobiles and restaurants moving together with retail trade as spending and consumer confidence improves. The University of Michigan's Index of Consumer Sentiment reports an index level of 95.0 for March 2015, which are pre-recession levels. I'll talk more about the index under macroeconomic data later. Going back to the charts, I broke out the consumer staples associated retail data which highlights the consumer staples' less volatile retail sales. The exception is the warehouse clubs and superstores group which grew rapidly before the Great Recession. I graphed volatile gasoline station sales separately from retail sales. Despite the current crude oil price slump, consumers are not spending their gas savings on other retailers.

Industry Level Data

Industry Data is supportive of growth as the National Retail Federation expects retail sales to grow 4.1% in 2015, on top of last year's growth of 3.5% last year. Although my charts below for Retail Trade and Food Services does include automobiles and restaurants, I see automobiles and restaurants moving together with retail trade as spending and consumer confidence improves. The University of Michigan's Index of Consumer Sentiment reports an index level of 95.0 for March 2015, which are pre-recession levels. I'll talk more about the index under macroeconomic data later. Going back to the charts, I broke out the consumer staples associated retail data which highlights the consumer staples' less volatile retail sales. The exception is the warehouse clubs and superstores group which grew rapidly before the Great Recession. I graphed volatile gasoline station sales separately from retail sales. Despite the current crude oil price slump, consumers are not spending their gas savings on other retailers.

Source: U.S. Census Bureau

Source: U.S. Census Bureau

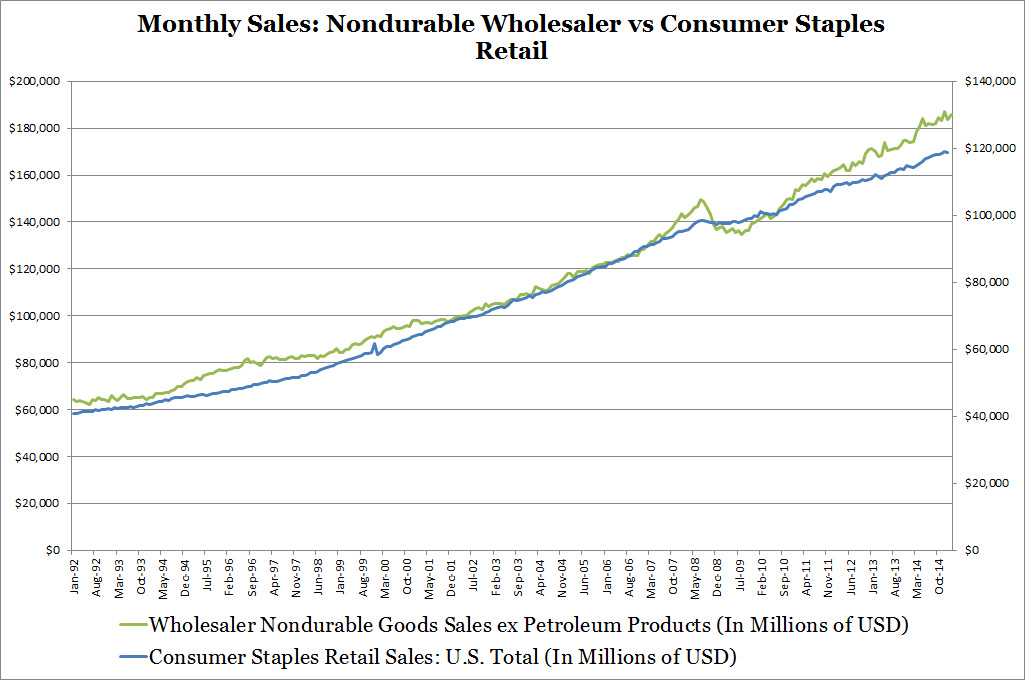

My Consumer Staples Industry Investment Model doesn't take into account retail sales directly because it's built on merchant wholesaler data. When I first created the model I saw a better fit with merchant wholesaler data. The reason is because many large consumer staples companies have their own distribution and warehouse networks regardless of whether they participate directly in retail sales. Their performance would more closely mimic wholesalers rather than retailers. I show below how similar nondurable wholesaler sales is compared to consumer staples retail sales.

Source: U.S. Census Bureau

Macroeconomic Data

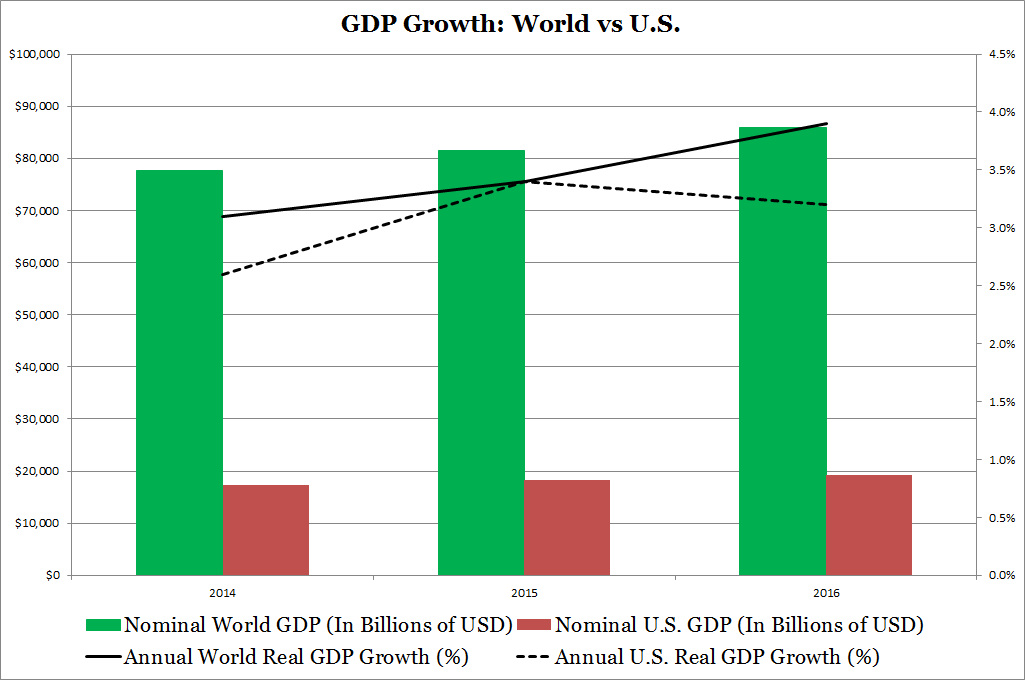

The Consumer Staples Select Sector SPDR ETF (XLP) as well as the S&P 500 contain many very large companies with global operations. The macroeconomic environment will have a larger impact on these companies. It's easy to get distracted by the U.S. dollar's rise, oil prices, and slowing world economies. The January 2015 International Monetary Fund's (IMF) GDP estimates include these global effects. The below shows that World Real GDP and U.S. Real GDP is increasing but U.S. growth slows in 2016.

The Consumer Staples Select Sector SPDR ETF (XLP) as well as the S&P 500 contain many very large companies with global operations. The macroeconomic environment will have a larger impact on these companies. It's easy to get distracted by the U.S. dollar's rise, oil prices, and slowing world economies. The January 2015 International Monetary Fund's (IMF) GDP estimates include these global effects. The below shows that World Real GDP and U.S. Real GDP is increasing but U.S. growth slows in 2016.

Source: International Monetary Fund

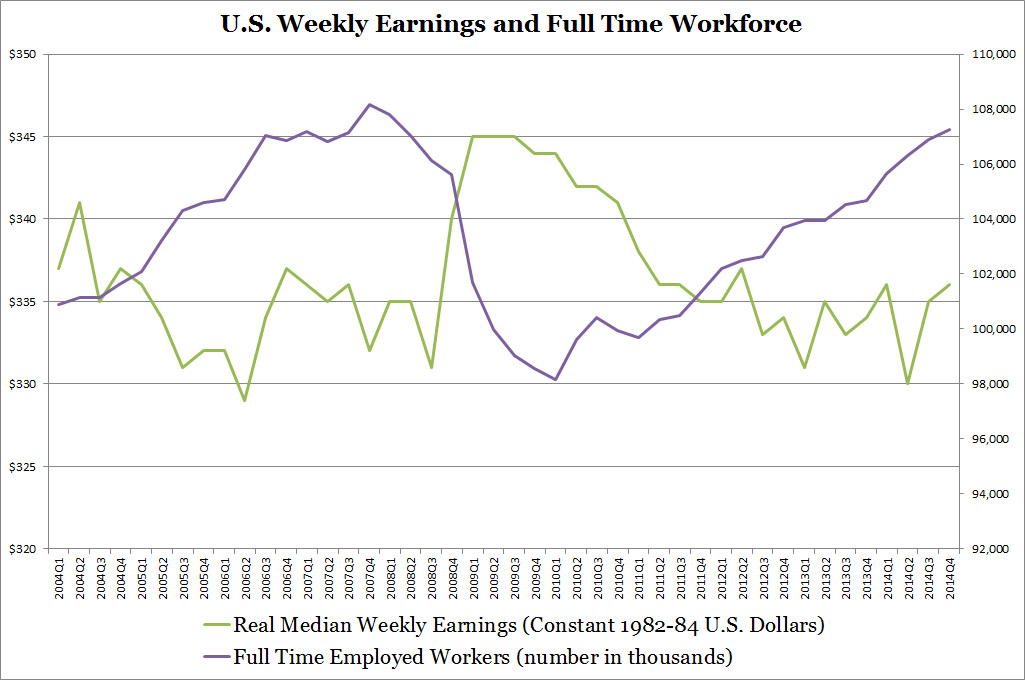

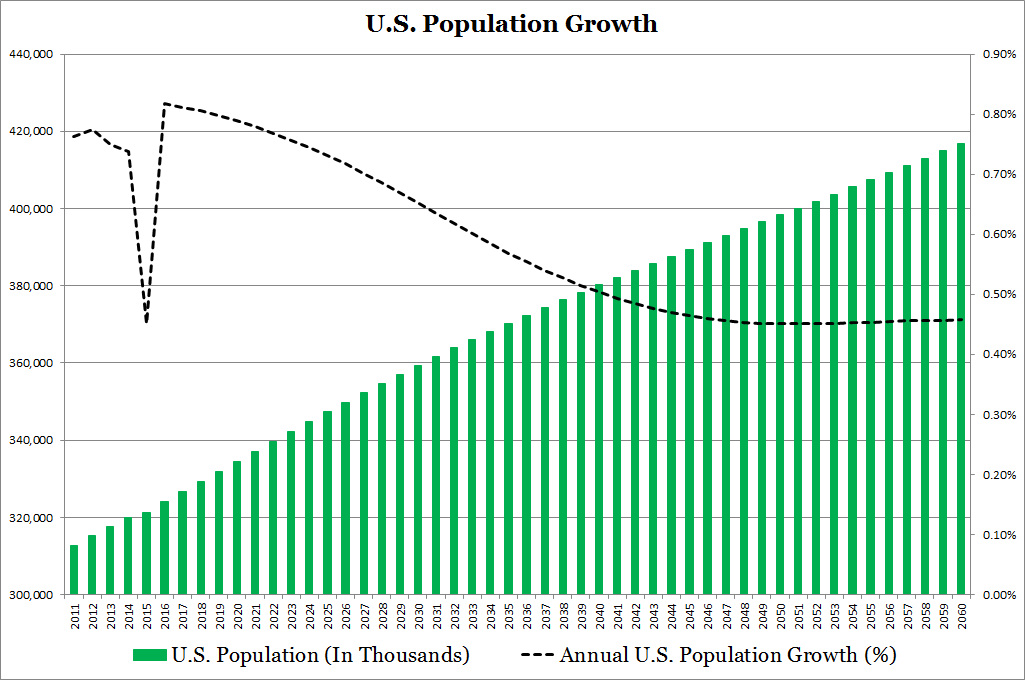

U.S. sales are still a significant part of consumer staples companies. Focusing on the medley of U.S. economic data in the two charts below, we see that despite a lack of growth in full time real median weekly earnings, the size of the full time workforce has almost increased back to pre-recession highs. This larger workforce provides more disposable income for a growing U.S. population to spend on consumer staples products. Despite the recent weak jobs report, it's important not to lose sight that job growth was positive. As future U.S. population growth in the far future slows, consumer staples stock performance may level off.

Source: U.S. Census Bureau

Source: U.S. Census Bureau

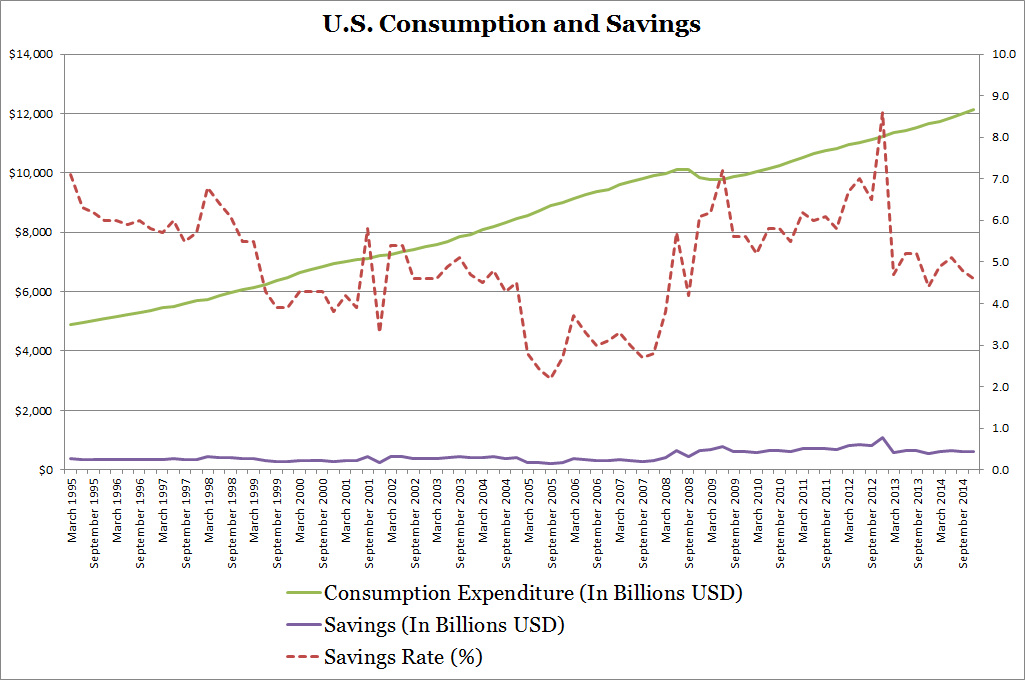

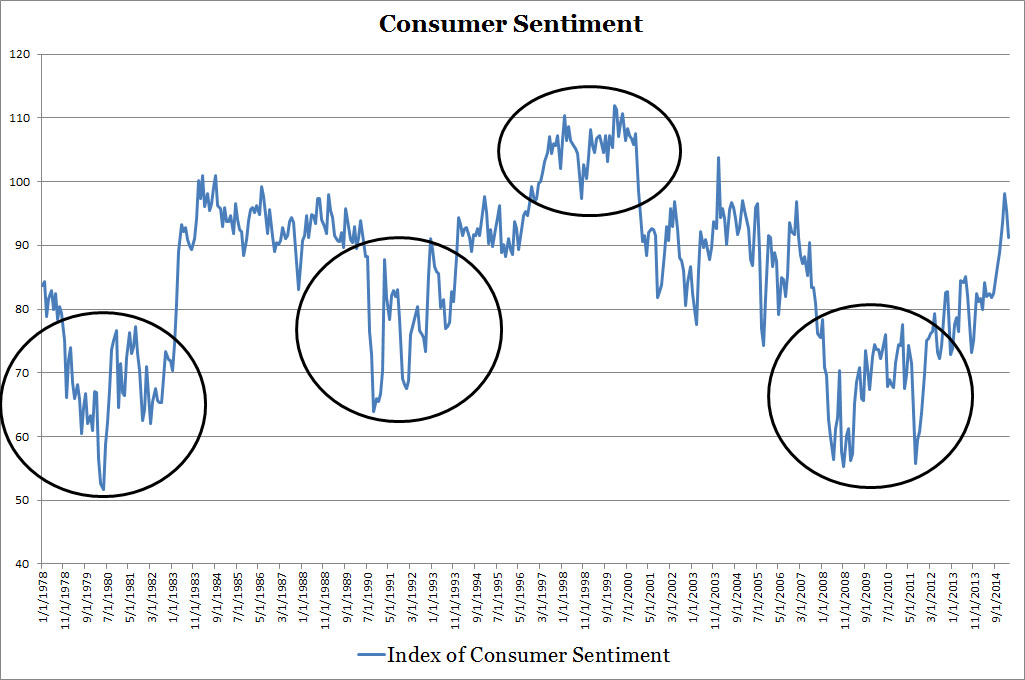

The charts below shows personal consumption expenditures, savings/savings rate, and consumer sentiment. Savings rate is inversely related to recessions while consumer sentiment moves with recessions. I would pay close attention to these indicators. Consumers are spending more as consumer sentiment is rising, this can be shown in the savings rate decline. The University of Michigan reports that for March 2015, consumer sentiment reached an all time high. In closing it mentions that consumer spending will rebound due to favorable job opportunities and that few consumers expect rising interest rates to hamper their purchases. This is great news for investors.

Source: Bureau of Economic Analysis

Source: University of Michigan

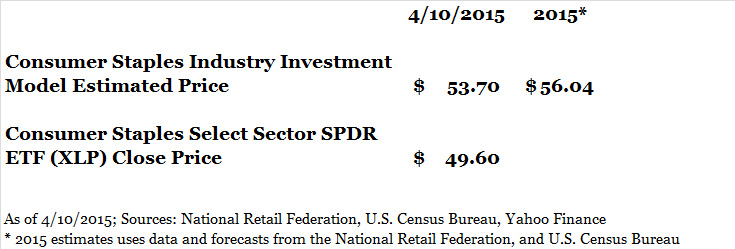

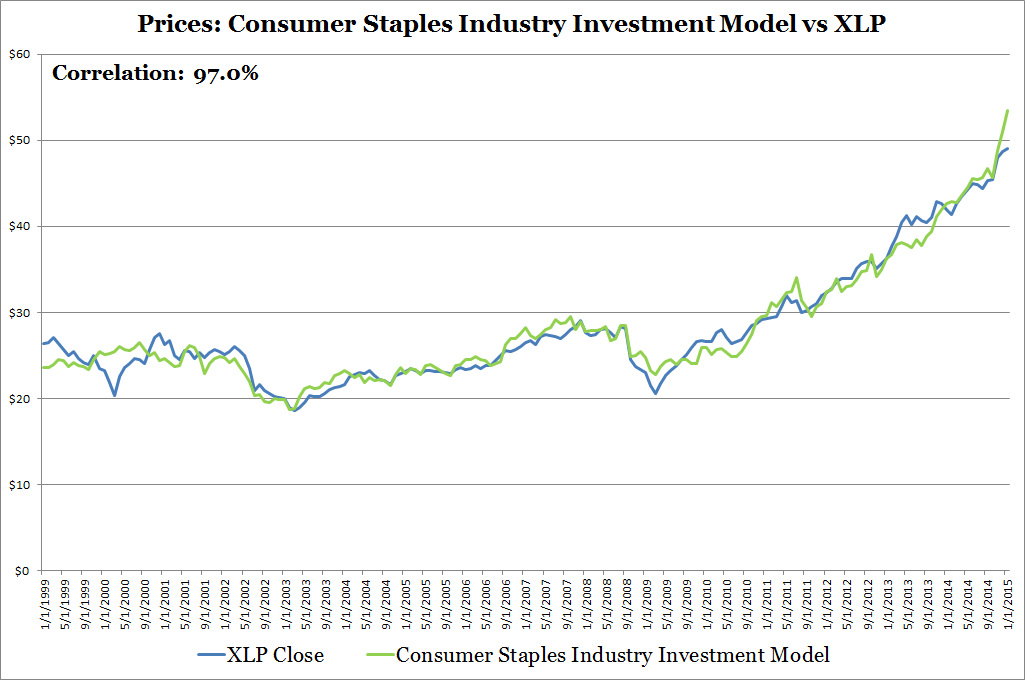

I'm excited that both industry and macroeconomic data are encouraging. After entering merchant wholesaler, National Retail Federation estimates of retail sales as a proxy for wholesaler sales growth, and general stock market (S&P 500) data into my Consumer Staples Industry Investment Model I calculate a mid $50 value for XLP. I also plotted historical XLP prices versus the Consumer Staples Industry Investment Model to show model accuracy. At the moment, I don't have a quantitative view of general stock market performance (S&P 500), but I'm working on a model that considers GDP and consumer sentiment data which can later be combined with the consumer staples model.

Sources: National Retail Federation, U.S. Census Bureau, Yahoo Finance

Is the Consumer Staples Industry Just Spinning Your Wheels?

My model estimates that the U.S. consumer staples industry is slightly undervalued based on current industry and macroeconomic data therefore the consumer staples industry as represented by XLP has room to grow. Because the S&P 500 is XLP's best friend, the stock market's volatility affects the consumer staples ETF's price. Luckily for both friends, the U.S. economy hasn't peaked. Consumer Sentiment has only been above 90 for four months but generally has to stay at a high level for an extended period of time before a recession comes along; also the savings rate hasn't fallen below 4%. Finally positive GDP growth from the IMF despite and positive U.S. economic data provides support.

Lastly, the consumer staples industry produces essential goods that will still be in high demand regardless of the economy making consumer staples stocks less volatile during economic downturns. If you're not convinced about my bullish view on the economy you should still consider having consumer staples stocks for your equity portfolio.

My model estimates that the U.S. consumer staples industry is slightly undervalued based on current industry and macroeconomic data therefore the consumer staples industry as represented by XLP has room to grow. Because the S&P 500 is XLP's best friend, the stock market's volatility affects the consumer staples ETF's price. Luckily for both friends, the U.S. economy hasn't peaked. Consumer Sentiment has only been above 90 for four months but generally has to stay at a high level for an extended period of time before a recession comes along; also the savings rate hasn't fallen below 4%. Finally positive GDP growth from the IMF despite and positive U.S. economic data provides support.

Lastly, the consumer staples industry produces essential goods that will still be in high demand regardless of the economy making consumer staples stocks less volatile during economic downturns. If you're not convinced about my bullish view on the economy you should still consider having consumer staples stocks for your equity portfolio.

RSS Feed

RSS Feed